"There is now liquidity at scale in private markets and that changes the picture for investors"

Market watch

"There is now liquidity at scale in private markets and that changes the picture for investors"

-

03 June 2026

-

Ardian

Reading time: 5 minutes

Vladimir Colas

Executive President

Vice-Chairman of the Executive Committee, Co-Chairman of the Operations Committee and Chairman of the ASF Management Committee, Vladimir Colas is also CEO of Ardian US and supervises several international Ardian subsidiaries, with a particular focus on the Americas. He also oversees Co-Investment, Private Credit and NAV financing activities, as well as the Group’s Finance, Compliance, Risk and Global Business Continuity Plan functions.

Vladimir Colas joined Ardian in 2003, starting his career in Paris in direct investment activities, then moving to secondary and primary activities. In 2006, he relocated to New York to accelerate the development of Ardian’s activities in the Americas, where the company now has 150 employees across 4 offices (New York, San Francisco, Santiago de Chile and Montreal).

Vladimir was instrumental in scaling Ardian's secondary business first in the Americas and then globally.

Vladimir Colas also co-founded the Ardian US Foundation, is a board member of the Ardian Foundation, and serves as a Member of the Board of Trustees of the Lycée Français of New York.

Private markets are seeing tremendous innovation. From broadening access to private assets and improving liquidity management to enabling GPs to hold high-quality assets longer, new tools have emerged that did not exist five years ago. One of the most significant consequences is the explosive growth of the secondary market. With more first-time sellers entering, we believe this is only the beginning, says Vladimir Colas.

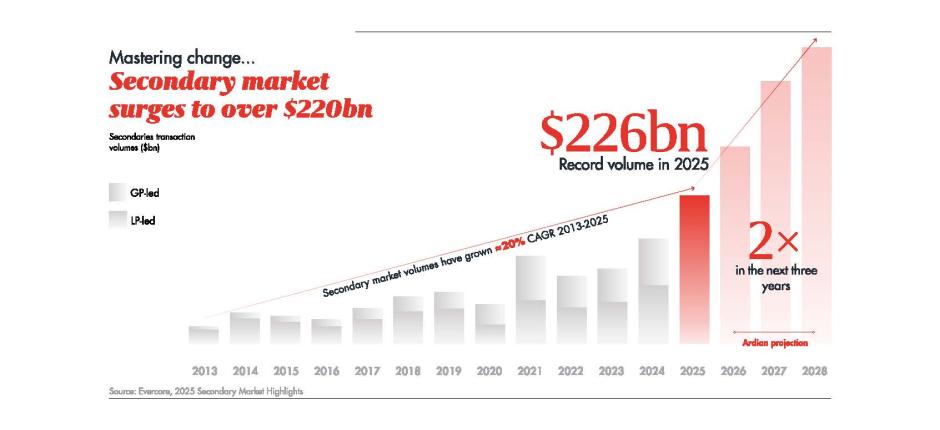

One of the most important changes for private markets is that more and more LPs are taking liquidity into their own hands, and are able to do so at scale. Over the past two to three years, exits have been delayed due to higher interest rates and geopolitical and market uncertainty. Portfolios have for the most part continued to perform with strong earnings growth, but with exits pushed back, some investors have found themselves structurally over-allocated. Unlike previous periods of volatility, such as the global financial crisis or Covid, when investors typically waited for over-allocation to unwind, LPs are now actively managing their portfolios by selling on the secondary market. The scale of the shift is clear: over the last two years, more than half of all sellers have been first-time sellers. In our experience, once LPs make a first sale, they quickly recognize the effectiveness of secondaries as a portfolio management tool and become recurring sellers. The result is that, even as exit conditions begin to improve, portfolio sales remain at record levels, supporting continued growth in secondary volumes. For us, this enables deployment at larger scale without being any less selective in what we buy.

-

23%

SAVC share of secondary market volume

-

c.20%

Growth in secondary market transaction volume, 2013-2025

Source: Evercore, 2025 Secondary Market Highlights

Single Asset Continuation Vehicles

Single asset continuation vehicles

Another area seeing rapid growth is single-asset continuation vehicles (SACVs). A SACV is a new fund created by a GP to continue to hold a single portfolio company already controlled through an older fund, while offering its investors the option to monetize their investment or to continue to hold. Today, SACVs account for around a quarter of the overall secondary market and are its fastest-growing segment. Last year, it grew by around 70% year on-year, generating more than $60 billion of deal flow – up from just $3 billion in 2018.What is driving this? While constrained liquidity plays a role, the primary driver is that GPs are reluctant to sell their highest-quality “compounders” to competitors. SACVs allow GPs to provide liquidity to existing investors while retaining ownership of their best assets. We see this in our own portfolio. Last year, our Expansion team completed its first continuation vehicle with Syclef. The team knew the asset well, had consolidated part of the market and saw a clear runway for further growth. After five years of ownership, however, keeping the asset in the existing fund was no longer appropriate. A SACV was therefore the right solution. Our view is that this market will continue to scale. We’ve already completed c.$800 million of transactions to date with very strong early performance, and have about $1 billion of available dry powder for this strategy. We are now focused on increasing our firepower over the next two years. One point that is often misunderstood is the risk profile. While these are single-asset transactions and therefore more concentrated, the risk is not comparable to a direct investment. A SACV is the continuation of an existing story: we, and the GP, are not discovering a business for the first time, but continuing to back a management team and an asset we have often followed for years via our unique database of 10,000+ private companies. As a result, downside risk is more limited, while upside potential remains attractive.

"We expect the secondary market to double again in the next three years."

Further growth ahead

Further growth ahead

The rise of first-time sellers and SACVs are two key drivers of a market that has seen truly dramatic growth and innovation over the past few years. Last year, the secondary market reached over $200 billion in deal volume for the first time – double the size it was only three to four years ago. In addition, the market continues to expand in other asset classes. In infrastructure secondaries, for example, the market has grown from $10 billion to $25 billion in just two years. At the same time, despite the industry raising larger funds, the secondary market remains undercapitalized: total dry powder available represents only around one year of deal volume. Taken together, these dynamics point to substantial further growth, and we expect the market will double again in the next three years. Despite this, barriers to entry are not coming down for our strategy. Information remains the name of the game: longstanding relationships with GPs, being a primary investor and spending time is essential to obtain the data required to be competitive. Finally, secondaries are attractive not only for their growth, but also for their risk-adjusted return profile. We have a loss ratio of less than 1% over more than 20 years, across approximately $50 billion deployed. In today’s market, that is something LPs appreciate.

Ardian's 2025 Integrated Report

Ardian’s 2025 Integrated Report outlines how we create long term value for investors, portfolio companies and society. Discover insights from our General Management Team on the key trends shaping private markets and Ardian’s distinctive approach to value creation.