LPs seek stability with European private credit

Market watch

LPs seek stability with European private credit

-

08 July 2026

-

Private Credit

Reading time: 5 minutes

Geopolitical uncertainty remains elevated, with effects that cut across all private investment strategies. But one consequence is clear: many LPs are now viewing Europe as a relative haven of stability.

Private credit highlights this trend particularly well. Latest fundraising figures show a significant re-weighting of LP interest toward the continent. This marks a clear shift from 2024, when much of the discussion centered on US exceptionalism.

European private credit: an attractive asset class in a volatile world

European private credit: an attractive asset class in a volatile world

One of the strengths of private credit as an asset class is its resilience to macroeconomic turbulence. This quality has become even more valuable in today’s context of heightened base-rate and inflation volatility. Because private credit is predominantly floating-rate and not subject to daily mark‑to‑market valuation, it has generally exhibited lower price volatility than more liquid markets such as high‑yield bonds and broadly syndicated leveraged loans, particularly during periods of rapid base‑rate and inflation volatility.

In Europe, private credit has continued to attract a growing investor base over time, irrespective of the prevailing macroeconomic environment. As an asset class, it is widely perceived as offering a stable risk-return profile, particularly when supported by disciplined underwriting and active portfolio management. Well-documented liquidity pressures within certain semi-liquid fund structures in the US market have, if anything, reinforced LP appreciation for the importance of appropriate alignment between fund structure and underlying asset liquidity. A principle that the most established European managers have long placed at the centre of their product design.

Within the mid-market, this approach is reinforced by a focus on through cycle business models providing mission critical products and services, where recurring revenues and predictable cash flows can potentially help limit sensitivity to broader economic fluctuations. The emergence of AI as a potential disruptor of established business models has added a further dimension to this analysis. Managers that have already embedded AI impact assessment into their initial underwriting and monitoring frameworks are increasingly well-placed to identify both the risks and the opportunities this creates, developing a clearer, more differentiated view of borrower resilience than those approaching the question reactively.

How did European private credit develop into such a resilient asset class – and what are the forces driving its growth today?

The rise of private credit: a structural, not cyclical driver

The rise of private credit: a structural, not cyclical driver

Before the 2008 global financial crisis, private credit in Europe was largely a subordinated debt opportunity, typically arranged by banks. In the years since, heightened regulatory pressure – most notably through the Basel III rules – has made banks less willing to hold illiquid loans to mid-market companies on their balance sheets.

This retrenchment created space for private credit funds to step in, fueling a decisive shift over the past decade toward direct lending. Today, direct lending represents the largest segment of the European private credit market, with activity concentrated predominantly in unitranche structures, which benefit from senior secured first liens.

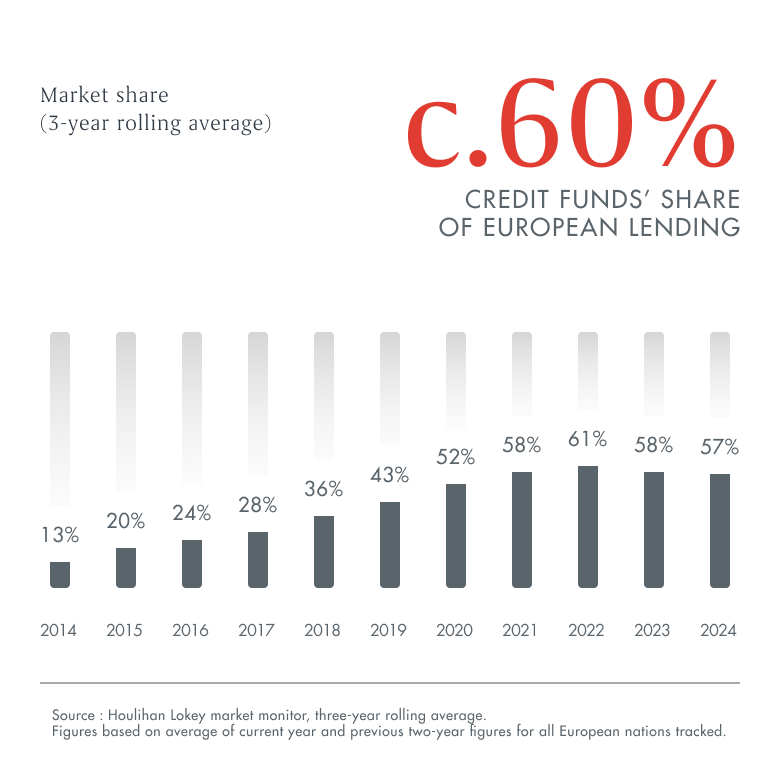

Bank retrenchment has opened space for private credit in Europe

With deal activity currently at historically high levels, a natural question is whether the market is entering a phase where growth will become more difficult.1Current evidence suggests that the expansion of private credit in Europe is structural rather than cyclical, reflecting a combination of post-crisis bank retrenchment, the progressive institutionalization of the asset class, and the accumulation of investor experience over time.

From an investor perspective, private credit has firmly established itself as a standalone asset class. The debates that followed the global financial crisis – around track record, resilience and longevity – have largely been resolved as the market has matured and demonstrated its ability to operate through multiple economic cycles.

This recognition has fueled sustained investor appetite, particularly for strategies that emphasize stability and disciplined risk management. In the present environment, marked by external uncertainty, the ability to navigate volatility and maintain consistent underwriting standards remains central to delivering an attractive risk-return profile.

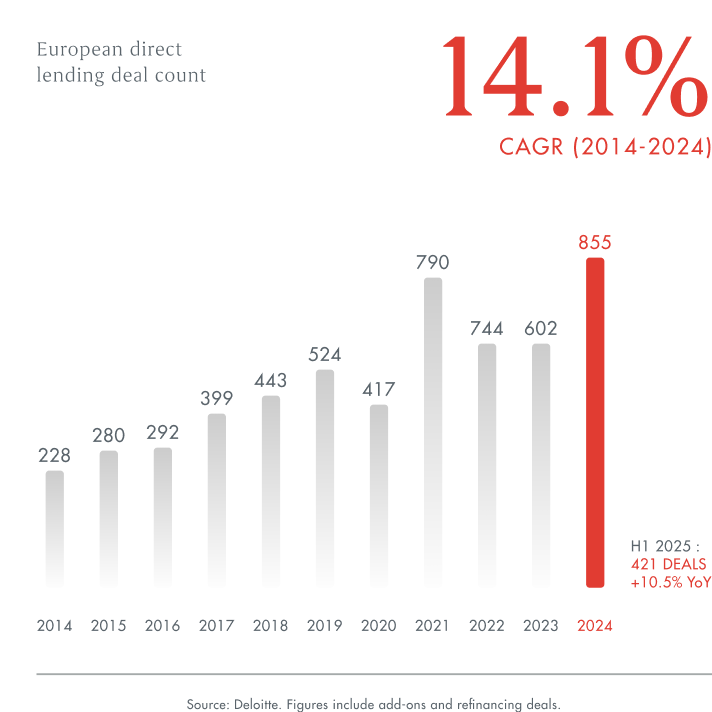

European direct lending activity remains elevated

Managers consolidate as the market matures

Managers consolidate as the market matures

After years of growth, the European private credit market is moving toward the $500bn AUM mark.2 It is also beginning to show signs of consolidation. This is evident as investors become more discerning, favoring managers with longer track records, experience navigating stress situations, and consistently low loss rates across cycles. Scale is also becoming a more meaningful factor, as only larger platforms can invest in the underwriting and risk-management capabilities required in a more complex environment and offer a broader range of financing options.

As a result, investors are concentrating allocations among a smaller pool of large and well-established managers. In this, European private credit is reflecting a broader consolidatory trend seen across the asset class worldwide, where incumbency and long-term experience confer a structural advantage.3

In this environment, the ultimate differentiator between managers will be fully realized performance over time.

Crystallizing performance: Ardian Private Credit

Crystallizing performance: Ardian Private Credit

>20-year track record | 0.03% | 0.44% |

in European private credit, delivering attractive risk-adjusted returns over multiple market cycles | Annualized realized loss rate, with 0% realized loss rate on first lien investments | Annualized default rate since inception – significantly lower than market average of 3.0% (Morningstar European Leveraged Loan Index, since 2007) |

1 Direct lending deal activity totaled €34bn as of October 2025 – nearly three time the level recorded in 2020. PitchBook, ‘European Private Credit Monitor,’ October 2025, p.5.

2 Preqin, ‘Global Report: Private Debt 2025,’ December 2024, p. 26.

3 Preqin, ‘Global Report: Private Debt 2025,’ December 2024, pp.15-16.