“In a consolidating market, scale matters”

Market watch

“In a consolidating market, scale matters”

-

03 June 2026

-

Ardian

Reading time: 4 minutes

Nicolò Saidelli

Advisor to Dominique Senequier on strategy and acquisitions

Nicolò Saidelli is Advisor to Dominique Senequier on strategy and acquisitions, Member of the Executive Committee and Head of Ardian Italy. Since joining Ardian in 2008, he has firmly established Ardian's presence in the Italian private equity market, while strengthening its strategic positioning in Europe.

Il is also Co-Head of Buyout and Member of the Buyout Management Committee. He played a decisive role in expanding this historic Ardian activity and developing transformative strategies to create global champions.

Prior to joining Ardian in 2008, he spent five years as a Partner with L Capital and Manager of its Italian office. He previously worked with GE Equity Italia, Salomon Smith Barney, Lehman Brothers, the Richemont Group, Canal Plus and Olivetti Group.

As the private equity industry matures, consolidation will continue to change the nature of the market. With investors increasingly favoring managers with scale, experience and a diversified offer, Ardian will prosper in this more selective environment, says Nicolò Saidelli.

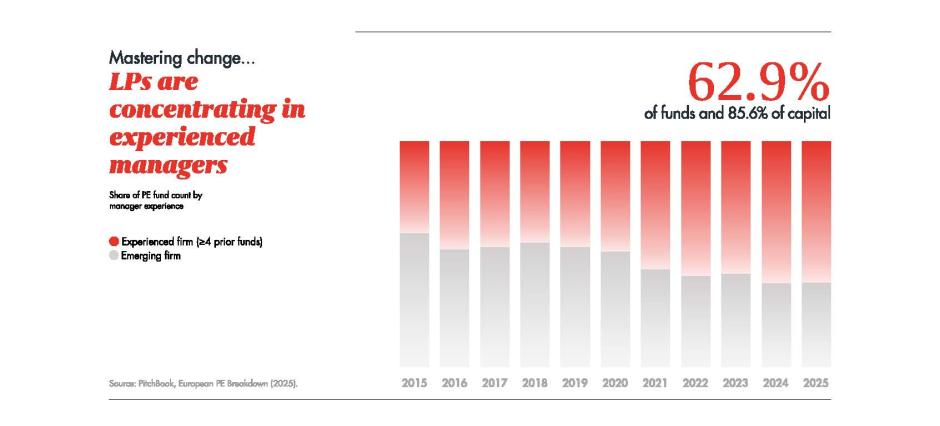

If you look at the private equity market today, consolidation is hard to miss. Hardly a week goes by without the press reporting a high-profile transaction between managers. These deals not only reflect a higher interest rate environment, but also a maturing industry in which capital is becoming more selective and managers must differentiate themselves through scale, execution and track record. This shift is clearly visible in fundraising dynamics. In Europe, capital is increasingly concentrated with established managers: last year, more than 85% of capital raised went to firms with at least four prior funds, according to PitchBook data. The logic is inescapable. Consolidation will continue, resulting in a more limited number of large platforms competing alongside highly specialized funds – with some players inevitably falling away.

-

c.40%

of European family-owned businesses except a leadership of ownership transition within the next decade

-

65%+

of Ardian Buyout deals have been with families and founders

Diversification: A survival imperative

Diversification: A survival imperative

This environment structurally favors Ardian. Managers need scale to build the central capabilities that are now essential and to remain relevant across major economic blocs. Diversification is equally critical. As investors consolidate relationships with fewer managers, they expect those platforms to offer a broad range of strategies. We see that many large firms that were historically focused on a single strategy – such as buyout – are now under pressure to diversify their product offering. We embraced diversification early in our evolution, growing organically to the 13 verticals that underpin our platform today. That does not mean we are a passive observer of this wave of consolidation. We remain vigilant and continue to assess opportunities, but in a disciplined and highly selective manner. Where it makes strategic sense, we may consider targeted acquisitions to strengthen areas where we are less scaled than some peers, while remaining fully scaled in areas such as infrastructure and secondaries. In a people business like ours, acquiring teams is not simply a matter of combining organizations: cultures must be aligned. We are therefore prepared not to proceed if the right cultural fit is not there.

“Our privileged access to families and founders is key to how we deliver attractive returns.”

Unique access to family businesses

Unique access to family businesses

Europe benefits from a dense fabric of successful mid-sized companies, often operating in niche markets and led by strong entrepreneurial teams. Today, 96% of companies with revenues above $100 million are privately held, meaning that investors seeking exposure to European growth are missing an opportunity if they restrict themselves to public markets.¹ At the heart of this opportunity are family-owned businesses. They account for more than 60% of all European companies, according to the European Commission, and succession is a recurring challenge across geographies. It is estimated that nearly 40% of European family-owned businesses expect a succession event within the next decade, creating a significant pipeline of opportunities.² Partnering with families has been a long-standing specialization for us – we have completed 36 family buyouts, and over 65% of our deals have been with families and founders. Our privileged access to these businesses and the primary nature of these deals are key to how we deliver attractive returns. This dynamic is reinforced by our deep local presence across Europe. In Italy alone, Ardian’s team of 60 has deployed more than $10 billion across its activities. Empowering teams locally was a key decision Dominique Senequier made early in our history. This proximity matters: you cannot deal with entrepreneurs if decisions are not made locally.

¹ Apollo Chief Economist, based on S&P Capital IQ data (2024).

² EY, ‘Family-Owned Businesses: The Role of Private Equity in Succession Planning,’ January 2025.

Ardian's 2025 Integrated Report

Ardian’s 2025 Integrated Report outlines how we create long term value for investors, portfolio companies and society. Discover insights from our General Management Team on the key trends shaping private markets and Ardian’s distinctive approach to value creation.